Systematic Investment Plan Calculator

| Year | Invested (₹) | Returns (₹) | Total Value (₹) |

|---|

| Month | Investment (₹) | Returns (₹) | Total Value (₹) |

|---|

What is an SIP Calculator?

Think of an SIP calculator as your personal financial simulator. It’s a simple yet powerful online tool that helps you estimate the future value of your investments made through a Systematic Investment Plan (SIP).

You just need to provide three basic inputs:

- The amount you wish to invest monthly (your SIP amount).

- The duration for which you plan to stay invested (the tenure).

- The expected annual rate of return on your investment.

In return, the calculator projects the total amount you will have invested, the potential wealth you could gain, and the estimated final maturity amount. It’s a crystal ball for your finances, helping you visualize how small, regular investments can grow into a substantial corpus over time.

How Does an SIP Calculator Work?

The magic behind an SIP calculator isn’t magic at all—it’s mathematics. The tool operates on the principle of compound interest. When you invest through an SIP, your money earns returns. The next month, you not only earn returns on your original investment but also on the returns gained previously. This cycle continues, creating a snowball effect where your money starts working for you.

An SIP calculator automates the complex formula for this calculation, instantly projecting the future value of your periodic investments. It takes your monthly investment and compounds it month after month over your entire investment tenure, giving you a clear picture of your financial growth.

How can an SIP Return Calculator Help You?

A good SIP return calculator is more than just a number-cruncher; it’s a goal-planning powerhouse. Here’s how it can help you:

- Goal-Oriented Planning: Do you want to accumulate ₹50 lakhs for a down payment in 10 years? An SIP calculator can help you determine the monthly SIP amount required to reach that target. It bridges the gap between your dreams and a tangible action plan.

- Motivation and Discipline: Seeing a projection of how your ₹10,000 monthly SIP could grow into a multi-crore retirement fund is incredibly motivating. It encourages you to stay disciplined and continue investing, even when the market is volatile.

- Making Informed Decisions: It allows you to experiment with different scenarios. You can see the impact of increasing your SIP amount by just ₹1,000 or staying invested for an extra 5 years. This helps you understand the power of time and consistency in wealth creation.

Benefits of Using an SIP Calculator

Using an SIP calculator before and during your investment journey offers numerous advantages:

- Financial Clarity: It eliminates ambiguity and provides a clear, quantifiable estimate of your future wealth.

- Saves Time and Effort: It performs complex calculations in a fraction of a second, saving you from tedious manual work.

- Free and Accessible: Most online platforms and mutual fund websites offer a free and user-friendly SIP calculator.

- Error-Free Results: Manual calculations are prone to human error. A digital calculator ensures accuracy.

- Empowers You: By understanding the potential outcomes, you feel more in control of your financial future and can make smarter investment choices.

How to Calculate SIP Returns?

Using an SIP calculator is incredibly straightforward. Here’s a simple step-by-step guide:

- Enter Your Monthly Investment: Input the amount you are comfortable investing each month (e.g., ₹5,000).

- Choose the Investment Period: Select the number of years you plan to stay invested (e.g., 10 years).

- Set the Expected Return Rate: Enter an estimated annual rate of return. For equity mutual funds, a long-term historical average might be around 12%, but remember this is just an assumption.

- Hit Calculate: The SIP calculator will instantly display your results, typically showing your total investment, estimated returns, and the total value.

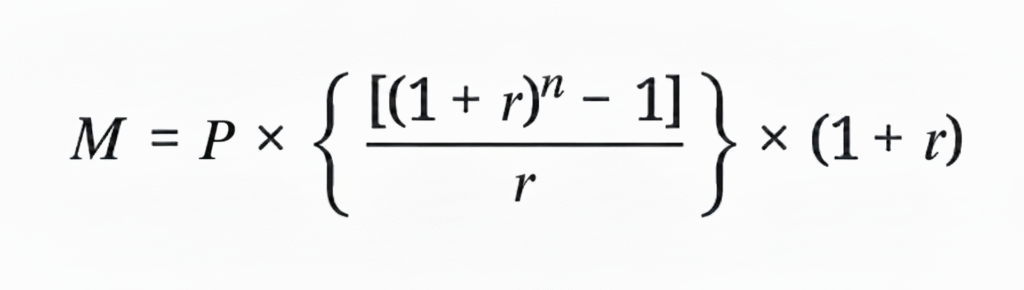

How Are SIP Investment Returns Calculated?

For those who love to see the mechanics, the calculation is based on the future value formula of an annuity. The SIP calculator uses the following formula to compute the final amount:

Where:

- M is the estimated maturity amount.

- P is the amount you invest per month via SIP.

- n is the number of months you will be investing.

- r is the expected monthly rate of return. (Note: The annual rate r is converted to a monthly rate, so r = r/12/100).

Types of SIPs

A Systematic Investment Plan (SIP) isn’t a one-size-fits-all product. To cater to the diverse needs of investors, fund houses offer several variations of SIPs. Understanding these types can help you choose the one that best aligns with your income, financial goals, and investment style.

- Regular SIP: This is the most common and straightforward type of SIP. You invest a fixed amount of money at regular intervals (usually monthly) for a predetermined period. It’s perfect for salaried individuals and those who prefer a disciplined, consistent approach to investing without any complexities.

- Top-Up SIP (or Step-Up SIP): This is a fantastic option for investors who expect their income to grow over time. A Top-Up SIP allows you to increase your investment amount by a fixed sum or a certain percentage at regular intervals (typically yearly). For example, you can start an SIP of ₹5,000 and set it to automatically increase by 10% every year. This small annual increment can significantly accelerate your wealth creation and help you reach your financial goals much faster.

- Flexible SIP (or Flexi SIP): As the name suggests, this SIP offers flexibility. It allows you to adjust your investment amount based on your financial situation or market conditions. If you have surplus cash in a particular month, you can invest more. If you’re facing a cash crunch, you can invest less or even skip an installment. This type is ideal for individuals with irregular income streams, like freelancers or business owners.

- Perpetual SIP: A regular SIP comes with a specific end date (e.g., 3 years, 5 years, etc.). A Perpetual SIP, however, does not have a defined tenure. The SIP continues indefinitely until you submit a request to the fund house to stop it. This is suitable for long-term goals like retirement, as it eliminates the hassle of renewing your SIP mandate and ensures your investment journey continues uninterrupted.

- Trigger SIP: This is a more advanced option for market-savvy investors. A Trigger SIP allows you to set specific conditions or “triggers” for your investment. For instance, you can set a trigger to invest a certain amount when the market index (like the Sensex or Nifty) falls by a particular percentage or when a fund’s Net Asset Value (NAV) drops to a level you’re comfortable with. It attempts to automate the process of buying low, but it requires a good understanding of market movements.

- Multi-SIP: Instead of setting up separate SIPs for different schemes within the same fund house, a Multi-SIP allows you to invest in multiple schemes using a single application and a unified payment instruction. This simplifies portfolio diversification and makes it easier to manage your investments within one Asset Management Company (AMC).

How to Choose the Right SIP Amount

Choosing the right SIP amount is crucial. Here’s a practical approach:

- Define Your Financial Goals: What are you saving for? A car? Retirement? Quantify the goal amount and the timeline.

- Assess Your Income and Expenses: Follow a budget to understand your disposable income. A popular rule is the 50/30/20 rule, where you allocate 20% of your income towards savings and investments.

- Work Backwards with a Calculator: Use a goal-based SIP calculator to determine the required monthly investment for your primary goal.

- Start Small, But Start Now: If the required amount seems too high, don’t be discouraged. The most important step is to start. Begin with an amount you are comfortable with and plan to increase it annually as your income grows.

Benefits of SIPs

Systematic Investment Plans have become incredibly popular, and for good reason. They offer a host of benefits that make investing accessible, disciplined, and effective for everyone, from beginners to seasoned investors.

- The Power of Compounding: This is perhaps the most significant benefit of SIPs. When you invest, your money earns returns. Over time, those returns also start earning their own returns. This creates a snowball effect, where your wealth grows at an accelerating rate. The longer you stay invested, the more powerful the effect of compounding becomes, turning small, regular investments into a substantial corpus.

- Rupee Cost Averaging: Timing the market is nearly impossible. SIPs eliminate this guesswork through a powerful concept called Rupee Cost Averaging. Since you invest a fixed amount regularly, you automatically buy more mutual fund units when the market is low (prices are down) and fewer units when the market is high (prices are up). Over the long term, this averages out your purchase cost and reduces the risk associated with market volatility.

- Instills Financial Discipline: By automating your investments, SIPs cultivate a habit of regular saving. A fixed amount is debited from your bank account each month, ensuring you invest consistently without having to make a conscious effort. This discipline is the bedrock of successful long-term wealth creation.

- Affordability and Accessibility: You don’t need a large sum of money to start investing. Most SIPs allow you to begin with as little as ₹100 or ₹500 per month. This low barrier to entry makes investing accessible to everyone, regardless of their income level. It empowers you to start your wealth creation journey early.

- Flexibility and Convenience: SIPs offer tremendous convenience. Once you set up an ECS/e-mandate, the process is completely automated. Moreover, you have the flexibility to increase, decrease, or even stop your SIPs at any point without incurring a penalty. This puts you in complete control of your investments.

Advantages of Using the AK Shah Finance SIP calculator

- Enables financial planning: The online SIP calculator by AK Shah Finance can assist you in financial planning. You can get an idea of how much you need to invest regularly to reach your target amount. This will help you in planning your monthly budget.

- Compare and assess SIPs: AK Shah Finance SIP Calculator helps you compare and assess various SIP investment strategies based on the final amount, total invested amount and the expected return.

- Free to access: AK Shah Finance Systematic Investment Plan Calculator is completely free to use, no matter how many times you use it. You can access the AK Shah Finance SIP Calculator at any time from anywhere in the world.

- Provides instant results: The investment calculator gives you instantaneous results that are accurate.

- Easy to use: The SIP MF Calculator by AK Shah Finance is easy to use. All you need to do is input the basic details of your SIP and get results in less than a minute.

- Full Information: After calculating the SIP, you can see the complete graph, annual growth and complete table to see how your money has grown.

Mistakes to Avoid in a Systematic Investment Plan

While SIPs are a powerful tool, certain common mistakes can undermine their effectiveness. Being aware of these pitfalls can help you stay on the right track and maximize your returns.

- Stopping SIPs During Market Downturns: This is the most common and costly mistake. When the market falls, many investors panic and stop their SIPs. However, a market dip is actually the best time to invest, as your fixed SIP amount now buys you more units at a lower cost. Stopping your SIP during a downturn is like getting out of the elevator just as it’s about to go up. Stay invested to reap the full benefits of rupee cost averaging when the market recovers.

- Not Aligning SIPs with Financial Goals: Investing without a clear purpose is like sailing without a destination. You should always link your SIP to a specific financial goal, whether it’s buying a house in 10 years, funding your child’s education, or building a retirement corpus. A clear goal keeps you motivated and helps you determine the right investment amount and tenure.

- Choosing the Wrong Fund: Don’t invest in a fund just because your friend recommended it or because it was a top performer last year. Your fund choice should be based on your risk appetite, investment horizon, and financial goals. Do your own research or consult a financial advisor to select a fund that aligns with your profile.

- Not Increasing Your SIP Amount Over Time: As your income grows, your capacity to invest also increases. Sticking with the same SIP amount for years can slow down your wealth creation. It’s crucial to periodically increase your SIP contribution. The best way to do this is by opting for a “Top-Up SIP,” which automatically increases your investment amount annually.

- Expecting Quick Returns: SIPs are designed for long-term wealth creation. The real magic of compounding and rupee cost averaging unfolds over several years. If you’re investing in equity SIPs, you should have an investment horizon of at least 5-7 years, if not longer. Chasing short-term gains can lead to disappointment and poor decision-making.

- Investing without an Emergency Fund: Life is unpredictable. Before you commit to an SIP, ensure you have an emergency fund that covers at least 6-12 months of your living expenses. This will prevent you from having to break your investments in case of an unexpected financial crisis, thereby protecting your long-term goals.

FAQs SIP Calculator

Are the results shown by an SIP calculator guaranteed?

No. The results are an estimation based on the expected rate of return you provide. Actual market returns can be higher or lower, as mutual fund investments are subject to market risks. The calculator is a tool for projection, not a guarantee.

What is a realistic expected rate of return to enter in the SIP calculator?

This depends on the asset class. For equity mutual funds, a long-term average of 10-12% is often used for calculations, based on historical performance. For debt funds, the rate would be lower. It’s wise to be conservative with your expectations.

Can I use an SIP calculator for any investment?

The SIP calculator is specifically designed for periodic investments like SIPs in mutual funds. It can also be used for recurring deposits (RDs) if you adjust the rate of return accordingly.

How often should I check my investments with an SIP calculator?

It’s best to use the calculator when you are planning your investments or doing an annual review of your financial goals. Avoid checking it too frequently, as short-term market fluctuations can cause unnecessary anxiety. Focus on the long-term picture.

What is the ideal duration for SIPs?

This is a great question, and the honest answer is: there is no single “ideal” duration for everyone. The right duration for your SIP depends entirely on your financial goals. The best practice is to align your SIP’s tenure with the timeline of the goal you are investing for.

Here’s a simple way to think about it:

- Short-Term Goals (1-3 years): If you’re saving for a goal like a vacation or a down payment on a bike, you might consider SIPs in lower-risk debt mutual funds. Equity SIPs are generally not recommended for such a short period due to market volatility.

- Medium-Term Goals (3-7 years): For goals like buying a car or funding a wedding, you could look at hybrid funds (a mix of equity and debt) which balance risk and return.

- Long-Term Goals (7+ years): This is where SIPs truly shine, especially in equity mutual funds. For major life goals like planning for your retirement, your child’s higher education, or building significant wealth, a long duration is crucial. A longer tenure (ideally 10, 15, or even 20+ years) allows you to ride out market fluctuations and fully leverage the incredible power of compounding.

Key Takeaway: For wealth creation through equity SIPs, the longer, the better. A minimum horizon of 7-10 years is often recommended to see meaningful results.

Can SIP returns be guaranteed?

No, the returns from an SIP are not guaranteed. This is a very important point to understand.

An SIP is simply a method of investing in a mutual fund; it is not an investment product itself. The returns you get are linked to the performance of the underlying mutual fund scheme you have chosen.

- If your SIP is in an equity mutual fund, its value will move up and down with the stock market. While there’s potential for high returns over the long term, there’s also the associated market risk.

- If your SIP is in a debt mutual fund, the risk is lower, but returns are still subject to changes in interest rates and are not guaranteed.

The reason SIPs are so popular is that they help manage this risk through Rupee Cost Averaging. By investing a fixed amount regularly, you automatically buy more units when the market is low and fewer when it is high. While this is a powerful strategy to average out your costs and reduce risk, it does not guarantee a specific rate of return.

How often should I review my SIPs?

While it’s tempting to check your investments every day, this often leads to anxiety and poor, emotionally-driven decisions. On the other hand, a “set it and forget it” approach isn’t ideal either.

A balanced approach is best. A yearly or semi-annual review is a healthy practice for most investors.

Here’s what you should look for during your review:

- Performance Check: Is your fund performing in line with its benchmark index (like the Nifty 50) and its peer funds in the same category? Don’t panic if there’s short-term underperformance, but consistent underperformance over 18-24 months might be a red flag.

- Goal Progress: Are you on track to meet your financial goal? As your income increases, consider using a “Top-Up SIP” to increase your monthly investment and reach your goal faster.

- Check for Fundamental Changes: Has there been a major change in the fund’s strategy or a change in the fund manager? This could be a reason to re-evaluate if the fund still aligns with your objectives.

- Review Your Own Financial Situation: Has your risk appetite or financial situation changed? A life event like a promotion or a new family member might require you to adjust your investment plan.

The key is to avoid knee-jerk reactions to market news and stick to a disciplined, periodic review schedule.