Inflation Calculator

Yearly Breakdown

| Year | Future Cost | Future Purchasing Power |

|---|

What Is an Inflation Calculator?

At its core, an Inflation Calculator is a simple yet powerful financial tool that shows you the changing value of money over a period. It helps you understand the purchasing power of a certain amount of currency in the past, present, or future. Think of it as a financial time machine that answers questions like, “What would ₹10,000 from the year 2005 be worth today?” or “If I want the same purchasing power as ₹1 Crore today, how much will I need in 2045?”

Why Understanding Inflation Matters for Your Finances

Ignoring inflation is like trying to fill a bucket with a hole in it. You might be saving money, but a silent force is constantly draining its value. Understanding inflation is crucial because it affects:

- Your Savings: Money kept in a low-interest savings account might actually be losing value every year.

- Your Budget: The cost of groceries, fuel, and utilities goes up, meaning your monthly budget needs to adapt.

- Your Salary: A 5% raise when inflation is at 7% is, in reality, a pay cut.

- Your Retirement Goals: The nest egg that seems huge today might be insufficient 20 years from now.

How Inflation Impacts the Value of Money Over Time

Let’s use a simple example. Imagine you have ₹100 today, and you can buy 10 cups of tea with it at ₹10 each.

Now, let’s say the annual inflation rate is 6%. Next year, the price of that same cup of tea will likely be ₹10.60. Your ₹100 note can now only buy about 9 cups of tea. The physical note is the same, but its purchasing power—what it can actually buy—has decreased. This erosion of value is the primary impact of inflation over time. An inflation calculator helps you quantify this exact loss.

What Causes Inflation?

Inflation isn’t just random; it’s caused by economic factors. The two main culprits are:

- Demand-Pull Inflation: This happens when demand for goods and services outstrips supply. Think of “too much money chasing too few goods.” When everyone wants to buy the latest smartphone, but there aren’t enough to go around, prices naturally rise.

- Cost-Push Inflation: This occurs when the cost of producing goods and services increases. For example, if global oil prices rise, the cost of transportation and manufacturing everything from plastics to food goes up, and companies pass these higher costs on to consumers.

The Effects of Inflation on Savings and Investments

This is where the rubber meets the road for your personal finances.

- On Savings: If your money is in a savings account earning 3% annual interest, but the inflation rate is 6%, you are experiencing a negative real return of -3%. Your money is growing, but its purchasing power is shrinking faster.

- On Investments: The primary goal of investing is to generate returns that beat inflation. If your investment portfolio yields 12% in a year when inflation is 6%, your real return is a positive 6%. You are genuinely growing your wealth. This is why investing is not just an option but a necessity for long-term financial health.

Historical Inflation Trends in India

India, like many developing economies, has experienced a dynamic history with inflation. Over the past few decades, we’ve seen periods of double-digit inflation as well as more controlled phases.

Typically, the Reserve Bank of India (RBI) aims to keep inflation within a target band, often around 2-6%. Historical data shows that an average long-term inflation rate of 5-6% is a reasonable assumption for future planning. A reliable Inflation Calculator uses this historical Consumer Price Index (CPI) data to provide accurate past-value calculations.

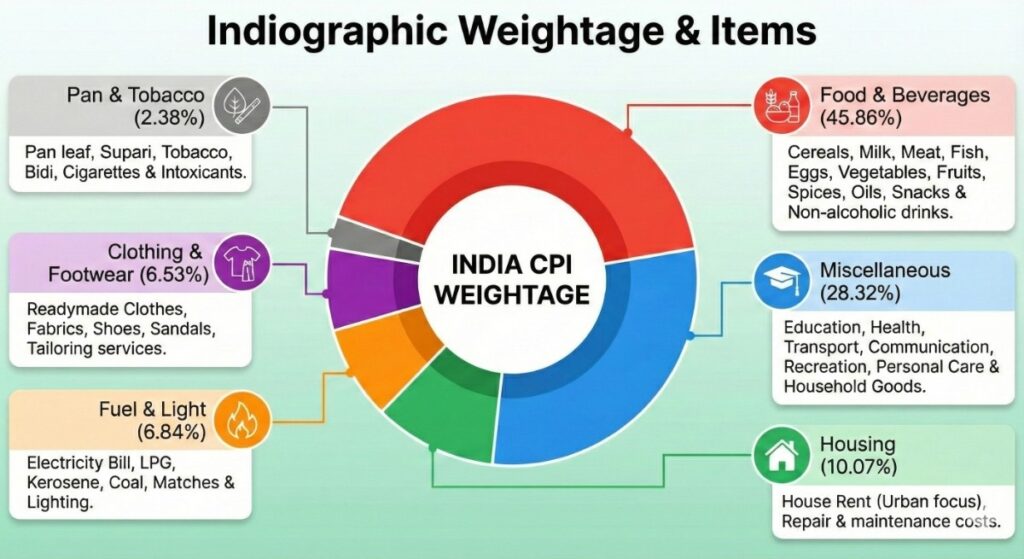

India CPI Weightages & Components

What Exactly Is an Inflation Calculator?

An inflation calculator is a financial tool that helps you understand how the purchasing power of money changes over time due to inflation.

In simpler terms, it tells you how much a certain amount of money in the past would be worth today, or how much today’s money will be worth in the future after accounting for inflation.

How to Use AK Shah Finance Inflation Calculator?

Using the AK Shah Finance Inflation Calculator is designed to be simple and intuitive. Here’s a step-by-step guide:

- Navigate to the website: Open the AK Shah Finance Inflation Calculator page on our website.

- Enter the Amount: In the “Present-Day Amount” field, type in the value you want to calculate.

- Annual Inflation Rate (%): Enter the per annum inflation rate in percentage

- Number of Years: Enter the period in years for which you want to understand the future price.

- Click “Calculate”: The calculator will calculate all the information you provide and display it to you.

How Inflation Calculators Help You Plan for the Future

An inflation calculator is a forward-planning powerhouse. Here’s how it helps:

- Retirement Planning: You think ₹2 Crore is enough for retirement in 30 years? Use the calculator to see what that amount will actually be worth. You might be surprised to find you’ll need ₹5 or ₹6 Crore to maintain the same lifestyle.

- Goal Setting: Planning for your child’s college education, which costs ₹20 Lakhs today? A calculator can project its likely cost in 15 years, helping you set a more realistic savings target.

- Insurance Coverage: It helps you determine if your life insurance cover is adequate for your family’s future needs.

How to Use Inflation Data for Better Financial Planning

Beyond just using an inflation calculator, you should integrate inflation data into your overall financial strategy:

- Benchmark Your Investments: Ensure your investment portfolio is consistently outperforming the average inflation rate.

- Negotiate Your Salary: Use inflation data as leverage when asking for a raise to ensure your income keeps pace with the cost of living.

- Adjust Your Budget: Review and adjust your household budget annually to account for rising costs.

Inflation vs. Investment Returns – Why It’s Important to Compare

This is one of the most critical concepts in finance.

- Nominal Return: The stated return on an investment. For example, a fixed deposit gives you a 7% return.

- Real Return: The return after accounting for inflation.

The formula is simple:

Real Rate of Return ≈ Nominal Rate of Return – Inflation Rate

If your nominal return is 7% and inflation is 6%, your real return is only 1%. You’ve only increased your purchasing power by 1%. This comparison is vital to understanding whether you are truly building wealth.

Planning Retirement with Inflation in Mind

Inflation is the biggest threat to a comfortable retirement. A fixed pension or a corpus that isn’t growing can be quickly eroded. When planning for retirement:

- Calculate Future Expenses: Use an inflation calculator to project your estimated annual expenses at the time of retirement.

- Build a Corpus that Beats Inflation: Invest in assets like equities and mutual funds that have the potential to deliver inflation-beating returns over the long term.

- Account for Medical Inflation: Remember that healthcare inflation is often higher than general inflation. Plan for it separately.

Challenges in Using Inflation Calculator

While incredibly useful, an inflation calculator has its limitations:

- It Uses Averages: The official CPI is an average. Your personal inflation rate might be higher or lower depending on your spending habits.

- Future Projections are Estimates: Projections for the future are based on an assumed average inflation rate, which may not hold true.

- It’s a Guide, Not Gospel: Use the results as a guideline to make informed decisions, not as an absolute certainty.

The Formula Underlying Inflation

The magic behind an inflation calculator is based on the future value formula. To find out what a certain amount of money (Present Value or PV) will be worth in the future (Future Value or FV), you use:

FV = PV x (1 + r)^n

Where:

- FV is the Future Value (the amount you’re solving for)

- PV is the Present Value (the initial amount)

- r is the annual inflation rate

- n is the number of years

This formula shows how the initial amount compounds with inflation year after year.

How Economists Calculate Inflation Rates (CPI, WPI, etc.)

Economists in India primarily use two indices to measure inflation:

- CPI (Consumer Price Index): As mentioned earlier, this tracks the retail prices of a basket of goods and services consumed by households. The RBI uses CPI as its key measure for monetary policy. This is the data most relevant to you and used by a personal inflation calculator.

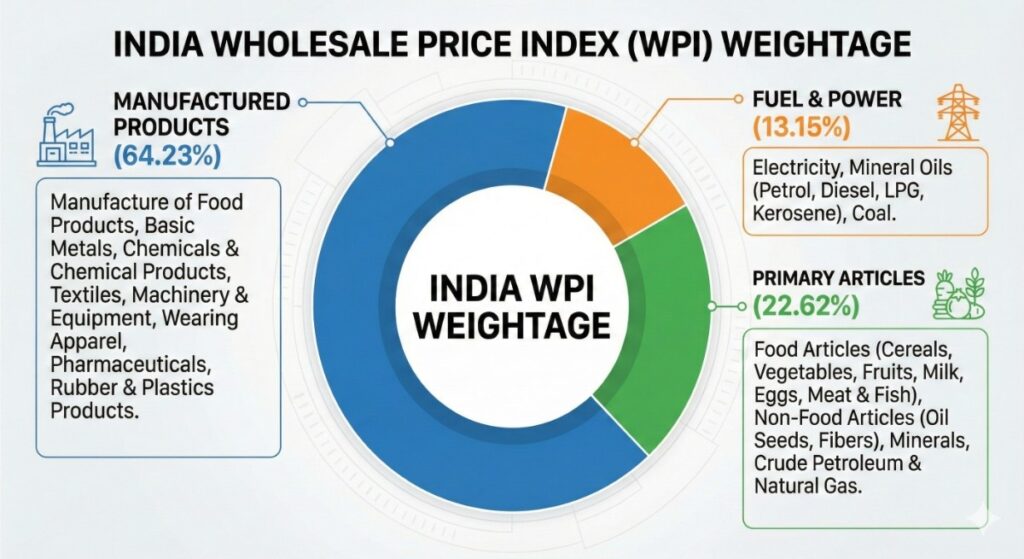

- WPI (Wholesale Price Index): This measures inflation at the wholesale level. It tracks the prices of goods before they reach the retail stage. It’s a key indicator for businesses and industry.

Why Everyone Should Use an Inflation Calculator Regularly

In today’s world, financial literacy is non-negotiable. Using an inflation calculator regularly should be a part of your financial hygiene because:

- It keeps you grounded in reality about the value of your money.

- It motivates you to save more and invest smarter.

- It helps you set financial goals that are realistic and achievable.

- It empowers you to have more meaningful conversations with a financial advisor.

A quick check-in once or twice a year can make a world of difference to your long-term financial security.

FAQs Inflation Calculator

Is an inflation calculator 100% accurate?

For historical calculations, it is highly accurate as it uses official CPI data. For future projections, it is an estimate based on an assumed inflation rate. Its accuracy depends on how close the assumed rate is to the actual future rate.

What is a good average inflation rate to use for future planning in India?

A long-term average of 5-6% is a common and reasonable assumption for financial planning in India. However, for specific goals like healthcare or education, it’s wise to assume a slightly higher rate (7-8%).

How is an inflation calculator different from a SIP calculator?

An inflation calculator shows you how the value of money decreases over time due to rising prices. A SIP calculator shows you how your money can grow over time through regular investments. They are two sides of the same coin: one measures the problem (inflation), and the other helps you find a solution (investing).

Can I use this calculator for other countries?

An inflation calculator is specific to a country’s inflation data. The AK Shah Finance calculator is calibrated for India using Indian CPI data. For other countries, you would need a calculator that uses their specific economic data.