Car Loan EMI Calculator

Results

| Loan Amount (₹) | Monthly EMI (₹) | Total Interest (₹) | Total of EMIs (₹) | Processing Fee (₹) | Total Outflow (₹) |

|---|

Your Amortization Details

| Period | EMI (₹) | Interest Paid (₹) | Principal Paid (₹) | Balance (₹) |

|---|

What Is a Car Loan EMI Calculator?

A Car Loan EMI Calculator is a simple online digital tool designed to help potential car buyers determine the specific amount they need to pay every month to the lender. “EMI” stands for Equated Monthly Installment.

Think of this calculator as a financial crystal ball. You input a few basic details—like how much money you want to borrow and for how long—and the tool instantly processes the numbers. It eliminates manual math errors and gives you a clear picture of your future financial commitment.

How can a Car Loan EMI Calculator Help You?

Using a Car Loan EMI Calculator isn’t just about finding out a single number; it is about financial planning. Here is how it helps:

- Budget Accuracy: It tells you exactly how much money will leave your bank account each month, helping you decide if you can afford that premium model or if you should stick to the base variant.

- Time-Saving: distinctive manual calculations can be tedious and prone to error. This tool gives instant results.

- Comparison Shopping: You can toggle between different interest rates from various banks to see which lender offers the most affordable deal.

- Debt Management: It breaks down the total amount payable, showing you how much of your money is going toward the principal versus how much is going toward interest.

How Does a Car Loan EMI Calculator Work?

The calculator works on a standard algorithm that factors in three primary inputs that you provide. To get a result from a Car Loan EMI Calculator, you usually need to adjust three sliders or enter three figures:

- Principal Amount (P): This is the total amount of money you wish to borrow from the bank.

- Interest Rate (R): The percentage rate at which the bank is lending you the money.

- Loan Tenure (N): The duration for which you are taking the loan (usually in months or years).

Once these are entered, the calculator applies the compound interest formula to generate your monthly payable amount.

Why You Should Use a Car Loan EMI Calculator Before Buying a Car

Many buyers make the mistake of walking into a dealership and focusing only on the “monthly payment” the salesperson quotes. Often, these quotes hide high-interest rates or extended tenures that make the car seem affordable but cost you a fortune in the long run.

By using a Car Loan EMI Calculator beforehand, you gain negotiation power. You walk in knowing exactly what you should be paying. It prevents you from overextending your finances and ensures your loan application doesn’t get rejected due to a poor debt-to-income ratio. It bridges the gap between your dream car and your real budget.

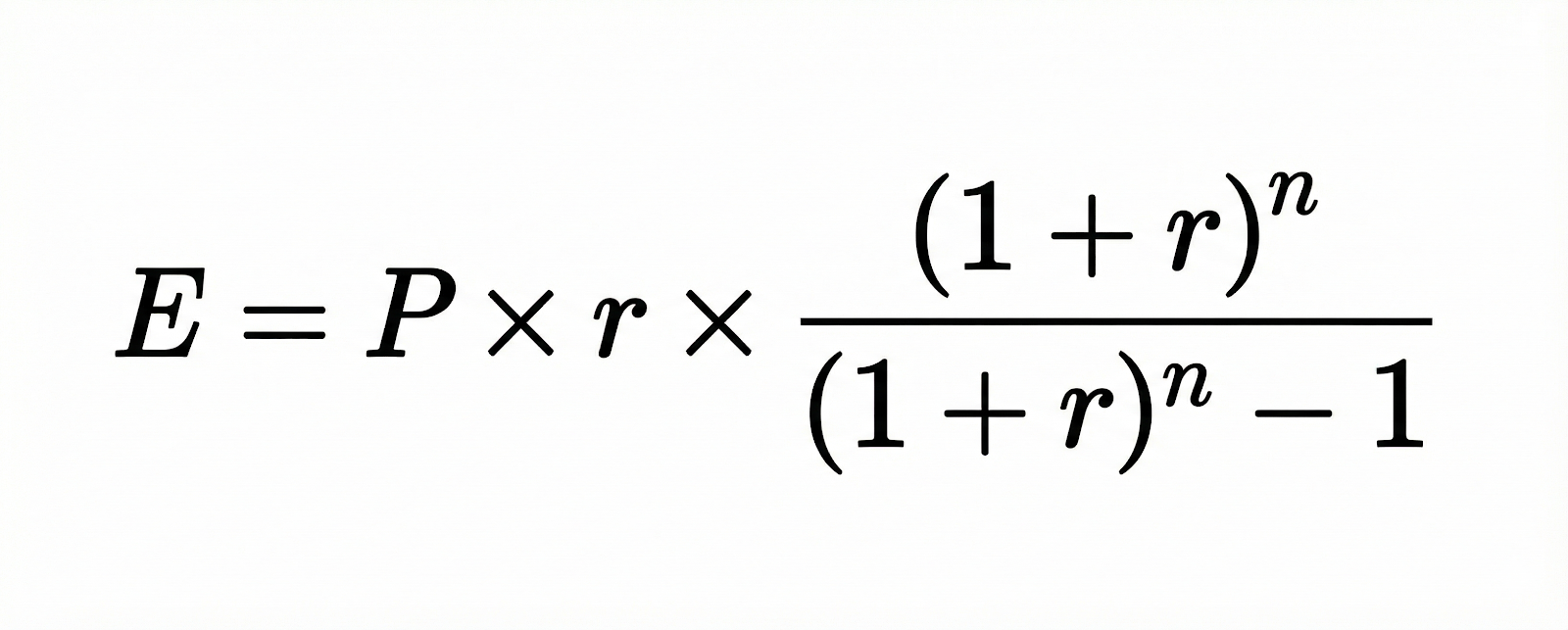

What Is The Formula To Calculate Car Loan EMI Amount?

While AK Shah Finance Car Loan EMI calculator does the heavy lifting in seconds, it is always good to know the math behind the magic. The standard mathematical formula used by a Car Loan EMI Calculator is:

Where:

- E = The EMI amount payable.

- P = The Principal loan amount.

- r = The monthly interest rate (Annual Rate divided by 12, then divided by 100).

- n = The loan tenure in months.

Example of Car Loan EMI Calculation

Let’s put the formula into a real-world perspective to see how a Car Loan EMI Calculator processes the data.

Imagine you want to buy a car and need a loan of ₹10,00,000. The bank offers you an interest rate of 9% p.a. for a tenure of 5 years (60 months).

- Principal (P): 10,00,000

- Rate (r): 9/12/100 = 0.0075

- Tenure (n): 60

Using the calculator, the result would be:

- Monthly EMI: ₹20,758

- Total Interest Payable: ₹2,45,501

- Total Payment (Principal + Interest): ₹12,45,501

This breakdown helps you realize that over 5 years, you are paying nearly ₹2.5 Lakhs just in interest.

How to Use AK Shah Finance Car Loan EMI Calculator?

Using this calculator is a simple process where you enter your loan details to get an instant breakdown of your repayment plan. Follow these steps based on the fields shown in the web page:

- Enter Car On-road Price:

- In the first field labeled “Car On-road Price (₹),” type the total price of the car you wish to buy.

- Enter Down Payment:

- In the “Down Payment (₹)” field, enter the amount you are paying upfront from your own pocket. The calculator will automatically subtract this from the car price to calculate your actual loan amount. If you are not paid down payment then put 0.

- Set Annual Interest Rate:

- Input the interest rate offered by your bank in the “Annual Interest Rate (%)” field.

- Set Loan Tenure:

- Enter the duration for which you want the loan in the “Loan Tenure” field.

- Select Tenure Type:

- Use the dropdown menu to select whether the tenure you entered is in “Years” or “Months.”

- Enter Processing Fee (Optional):

- If your bank charges a fee to process the loan, enter the percentage in the “Processing Fee (% of Loan Amount)” field (e.g., 1) if not applicable then put 0.

- Choose Amortization View:

- Select “Yearly” or “Monthly” from the dropdown to decide how you want to see your repayment schedule detailed at the bottom.

- Click Calculate:

- Hit the green “Calculate” button. The results will instantly appear below in the “Results” section, showing your Monthly EMI, Total Interest, and Total Outflow.

Factors That Affect Your Car Loan EMI

When you play around with a Car Loan EMI Calculator, you will notice that the EMI changes based on several variables:

- The Loan Amount: The higher the loan, the higher the EMI.

- Interest Rate: Even a 0.5% difference can significantly change your monthly outflow.

- Loan Tenure: A shorter tenure means higher EMIs but lower total interest. A longer tenure reduces the monthly EMI but increases the total interest cost.

- Credit Score: A high credit score can help you negotiate a lower interest rate, directly reducing your EMI.

Fixed vs Floating Interest Rate for Car Loans

When taking a loan, you might encounter two types of interest rates.

- Fixed Interest Rate: The rate remains the same throughout the loan tenure. Your EMI will not change, regardless of market fluctuations. This is great for predictability.

- Floating Interest Rate: The rate is linked to a benchmark (like the Repo Rate). If the market rates drop, your interest burden decreases. However, if rates rise, your EMI could go up.

Most car loans are offered at fixed rates, but it is essential to check this before signing, as it changes how the Car Loan EMI Calculator forecasts your future payments.

How to Choose the Right Car Loan for You

A low EMI isn’t the only definition of a “good” loan. When choosing a lender:

- Compare the APR: Look at the Annual Percentage Rate, not just the advertised interest rate.

- Check LTV (Loan to Value): Some banks fund 100% of the on-road price, while others only fund 80% of the ex-showroom price.

- Processing Fees: Ensure the low interest rate isn’t accompanied by a massive processing fee.

- Foreclosure Charges: If you plan to pay off the loan early, choose a bank with low or zero foreclosure charges.

How to Reduce Your Car Loan EMI

Is the number shown on the Car Loan EMI Calculator too high for your comfort? Here is how you can bring it down:

- Increase the Down Payment: The more you pay upfront, the less you need to borrow. This is the most effective way to shrink your EMI.

- Correct Tenure Selection: Extending the tenure reduces the monthly burden (though it increases total interest).

- Negotiate the Rate: If you have a credit score above 750, negotiate with the bank for a better rate.

- Step-down EMI: Some banks offer loans where EMIs start high and reduce over time as the principal decreases.

Common Mistakes to Avoid When Taking a Car Loan

Even with a Car Loan EMI Calculator, buyers make mistakes:

- Borrowing More Than Needed: Just because you are eligible for a 20 Lakh loan doesn’t mean you should take it. Stick to your needs.

- Ignoring the “On-Road” Price: Calculators often use the showroom price. Remember to factor in insurance, registration, and taxes into your loan amount.

- Forgetting Total Interest: Don’t just look at the monthly ₹15,000 payment. Look at the total interest. If the interest cost is 40% of the car’s value, it might be a bad financial decision.

Advantages of Using AK Shah Finance Online EMI Calculator for Car Loans

According on the features visible in the web page, here are the key benefits of using this specific tool:

- Comprehensive Financial Breakdown:

Unlike simple calculators that just show the EMI, this tool gives you a detailed summary including:

- Loan Amount: The actual amount you are borrowing after the down payment.

- Total Outflow: The combined total of your loan, interest, and processing fees, so you know the true cost of the car.

- Processing Fee Calculation: It explicitly calculates the processing fee value, which is often a hidden cost users forget to account for.

- Visual Analysis (Charts & Graphs):

- Pie Chart: It provides a clear visual split between your “Principal” and “Total Interest,” helping you see how much of your money is going towards the bank’s profit versus paying for the car.

- Line Graph: The reducing balance graph shows visually how your loan balance will decrease over time.

- Detailed Amortization Schedule:

- The “Your Amortization Details” table at the bottom is a huge advantage. It breaks down your payments year-by-year, showing exactly how much interest and principal you pay annually, and what your year-end balance will be. This helps in planning future pre-payments.

- Flexible Tenure Options:

- The option to toggle the “Tenure Type” between years and months allows for precise calculations, especially if you are planning for a short-term loan that doesn’t fit into perfect year blocks.

- Instant “On-Road” Adjustment:

- By asking for the “Car On-road Price” and “Down Payment” separately, it automatically does the math to find your required loan amount, saving you from doing manual subtractions before using the tool.

FAQs Car Loan EMI Calculator

Is the result from a Car Loan EMI Calculator 100% accurate?

It is mathematically accurate based on your inputs. However, banks may add processing fees or service taxes that slightly alter the final disbursement.

Does checking the calculator affect my credit score?

No. Using an online calculator is a “soft inquiry” and has zero impact on your credit score.

Can I use this calculator for used cars?

Absolutely. The logic remains the same, though interest rates for used cars are typically higher than for new cars.

What happens if I make a part-payment?

Making a part-payment reduces your principal amount. This will either reduce your subsequent EMIs or shorten your loan tenure.

Does the Car Loan EMI Calculator account for “Flat Interest Rates”?

AK Shah Finance Car Loan EMI calculator uses the “Reducing Balance” method, which is the standard used by major banks. Be careful—dealerships sometimes quote a “Flat Interest Rate” to make the deal look cheaper. If you plug a Flat Rate number into a standard Car Loan EMI Calculator, the results won’t match because a Flat Rate results in a much higher effective EMI than a Reducing Balance rate.

Does the calculator include costs like car insurance and road tax?

No, the calculator only processes the loan amount. However, if you plan to take a loan that covers 100% of the on-road price (which includes insurance and tax), simply enter that total figure as your “Principal Amount” to get an accurate calculation.

How does a “Zero Down Payment” scheme affect the results?

If you opt for zero down payment, your Principal (P) increases significantly. If you enter the full car price into the Car Loan EMI Calculator, you will likely see a steep rise in your monthly outgoing and a massive increase in the total interest paid over the years.

Why doesn’t the EMI amount match the one my bank manager told me?

The Car Loan EMI Calculator gives you the pure mathematical figure. Banks sometimes include “Loan Protection Insurance” or add the “Processing Fee” into the loan amount, which slightly increases the EMI. Always ask the bank for a breakdown if the numbers don’t align.

Can I use this calculator for a lease agreement?

Generally, no. A car lease works differently than a loan. A lease payment pays for the depreciation of the car, whereas a Car Loan EMI Calculator is designed to pay off both the principal and interest to eventually give you ownership of the vehicle.

Does the loan start date affect the calculation?

The EMI amount usually remains the same regardless of the start date. However, the date you pay (beginning of the month vs. end of the month) might slightly affect the interest calculation in the very first or last month, depending on the bank’s specific policy.