Systematic Withdrawal Plan Calculator

What is an SWP (Systematic Withdrawal Plan)?

Think of a Systematic Withdrawal Plan (SWP) as a reverse SIP (Systematic Investment Plan). Instead of investing a fixed amount of money every month into a mutual fund, an SWP allows you to withdraw a fixed amount of money from your mutual fund investment at regular intervals (monthly, quarterly, etc.).

It’s a smart way to create a regular cash flow from your lump-sum investment, much like receiving a pension or a salary. This is especially useful for retirees who need a steady stream of income to cover their living expenses.

How Does an SWP Work?

The mechanism is quite straightforward. Let’s say you have invested a significant amount in a mutual fund scheme.

- You Invest: You start with a lump-sum investment in a mutual fund (usually a debt or hybrid fund for stability).

- You Decide the Withdrawal: You instruct the fund house about the amount you wish to withdraw and the frequency (e.g., ₹10,000 every month).

- Units are Redeemed: On the specified date, the fund house redeems the equivalent number of mutual fund units to provide you with your fixed amount.

- Money is Credited: This amount is then transferred directly to your bank account.

The remaining units in your investment continue to stay invested, potentially growing over time and generating returns that can fund your future withdrawals.

What is an SWP Calculator?

An SWP calculator is an online financial tool designed to help you plan and visualize your systematic withdrawals. It helps you estimate how long your investment corpus will last based on your withdrawal amount, expected rate of return, and total investment.

Think of it as a simulator for your financial future. By inputting a few key details, this calculator projects the entire cash flow, showing you the opening balance, withdrawal amount, investment growth, and closing balance for each period until the end of your chosen tenure. Using an SWP calculator takes the guesswork out of planning your income stream.

Why You Should Use an SWP Calculator

Planning for a regular income from your investments isn’t something you should leave to chance. Here’s why using an SWP calculator is a non-negotiable step:

- Goal Clarity: It helps you determine a sustainable withdrawal amount that aligns with your financial goals.

- Corpus Longevity: The biggest fear for any retiree is outliving their savings. The calculator shows you if your corpus will last for the desired duration.

- Informed Decision Making: You can experiment with different withdrawal amounts and tenure to find the perfect balance that suits your needs.

- Avoids Over-withdrawal: It prevents you from withdrawing too much too soon, which could deplete your principal amount faster than you’d like.

How to Use an SWP Calculator Step-by-Step

Using an SWP calculator is incredibly easy. Most online tools require you to enter the following four inputs:

- Initial Investment Amount: This is the lump-sum amount you plan to invest (e.g., ₹10,00,000).

- Withdrawal Amount (per month): The fixed amount you wish to receive every month (e.g., ₹10,000).

- Expected Annual Return (%): The realistic rate of return you expect your mutual fund investment to generate per year (e.g., 8%).

- Investment Period (in years): The duration for which you plan to make these withdrawals (e.g., 20 years).

- Withdrawal Frequency: When do you want to withdraw money from SWP — Monthly, Quantity, Half-Yearly or Yearly (e.g., Monthly).

- Expected Inflation Rate (%): You can enter the Inflation rate as per your requirement or you can enter zero (e.g., 6).

Once you input these values and hit ‘Calculate’, the SWP calculator will instantly provide you with a detailed summary, including the total amount withdrawn and the final value of your investment at the end of the tenure.

Example: Calculating SWP Returns

Let’s put the SWP calculator to work with a practical example.

Meet Mrs. Gupta, a 60-year-old retired teacher.

- Total Initial Investment: ₹30,00,000

- Monthly Withdrawal: ₹25,000

- Expected Annual Return: 7%

- Tenure: 15 years

- Expected Inflation rate (%): (e.g.,0)

Upon entering these details into an SWP calculator, Mrs. Gupta would see the following results:

- Total Amount Withdrawn: ₹45,00,000 (₹25,000 x 12 months x 15 years)

- Final Corpus of Investment: Approximately ₹6,22,783

This simple calculation shows Mrs. Gupta that not only can she comfortably withdraw ₹25,000 per month for 15 years, but her initial capital will also remain almost intact, thanks to the power of compounding.

Benefits of Using an SWP Calculator

Beyond basic calculations, a good SWP calculator offers several benefits:

- Accuracy: It performs complex calculations instantly, eliminating the risk of manual errors.

- Scenario Analysis: You can easily compare different scenarios. What if the return is 6% instead of 7%? What if you withdraw ₹30,000 instead of ₹25,000? A calculator lets you see the impact of these changes in seconds.

- Free and Accessible: AK Shah Finance Systematic Withdrawal Plan Calculator is completely free to use, no matter how many times you use it. You can access the AK Shah Finance SWP Calculator at any time from anywhere in the world.

- Better Financial Planning: It provides a clear roadmap, empowering you to plan your post-retirement life with confidence.

Things To Keep In Mind Before Investing In an SWP

While an SWP is a fantastic tool, it’s essential to be aware of a few things:

- Market Volatility: The returns are not guaranteed and are subject to market risks. If the market performs poorly, your fund may have to redeem more units to pay you, depleting your corpus faster.

- Taxation: The money you withdraw via SWP is treated as a redemption and is subject to Capital Gains Tax. For equity funds, if units are sold within a year, Short-Term Capital Gains (STCG) tax is applicable. If sold after a year, Long-Term Capital Gains (LTCG) tax applies. Similar rules apply to debt funds with different holding periods.

- Exit Load: Some mutual fund schemes charge an exit load if you redeem units before a specified period (usually one year). Plan your SWP to start after this period to avoid unnecessary charges.

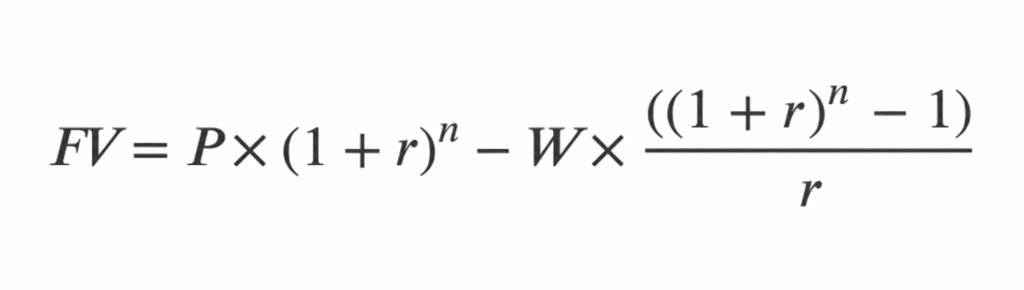

What is the SWP Calculator Formula?

While AK Shah Finance SWP calculator does the work for you, it’s interesting to know the logic behind it. The calculation is typically an iterative process, but it can be represented by a formula that calculates the future value of your investment after ‘n’ withdrawal periods.

The formula for the final value (FV) of your investment is:

Where:

- FV = Future Value (the amount left after the tenure)

- P = Initial Principal Investment

- W = Withdrawal Amount per period

- r = Rate of return per period (annual rate / number of periods in a year)

- n = Total number of withdrawal periods (years x number of periods in a year)

This formula looks complex, which is precisely why an SWP calculator is so handy!

How Does An Online SWP Calculator Help?

The AK Shah Finance SWP calculator takes into account factors such as compounding returns, the impact of regular withdrawals on the investment’s principal, and the potential growth of the remaining invested amount. It provides users with a clear understanding of how their investments may fare over time and allows for adjustments to be made based on their financial objectives and risk tolerance.

The output from AK Shah Finance SWP calculator empowers investors to assess the viability of their withdrawal plans, adjust withdrawal amounts, tenure, or investment allocations if needed, and ensure that their investments can sustain their desired income stream over the long term.

It is important to note that while an online Systematic Withdrawal Plan calculator provides valuable insights, actual investment returns may vary due to market fluctuations and other factors. Therefore, it is important to consult with a financial advisor or professional to tailor the SWP strategy to individual financial goals and circumstances.

SWP vs SIP: What’s the Difference?

People often confuse SWP with SIP, but they are polar opposites.

| FEATURE | SWP (Systematic Withdrawal Plan) | SIP (Systematic Investment Plan) |

|---|---|---|

| Cash Flow | Inflow (Money comes from the fund to your Bank) | Outflow (Money goes from your bank to the fund) |

| Purpose | Income Generation / Utilizing a Corpus | Wealth Accumulation / Building a corpus |

| Who is it for? | Investors needing a regular income, like retirees. | Investors looking to build wealth over time |

| Process | Selling mutual fund units regularly | Buying mutual fund units regularly |

Who Should Use an SWP?

SWP is an ideal solution for:

- Retirees: The most common users, who need a fixed income to replace their salary.

- Individuals on a Sabbatical: To cover expenses during a planned career break.

- Those Seeking a Second Income: To supplement their primary salary with an additional, passive income stream.

- Parents: To fund a child’s regular educational or living expenses from a dedicated investment.

Common Mistakes to Avoid When Using an SWP Calculator

To get the most accurate picture, avoid these common pitfalls:

- Being Overly Optimistic: Do not input an unrealistically high expected rate of return. It’s better to be conservative.

- Ignoring Inflation: A withdrawal of ₹20,000 today won’t have the same purchasing power 10 years from now. Consider increasing your withdrawal amount periodically to account for inflation.

- Setting a High Withdrawal Rate: Withdrawing too high a percentage of your corpus (e.g., over 8-10% annually) can erode your capital very quickly, especially in volatile markets.

- Forgetting Taxes: The results from the SWP calculator are pre-tax. Always factor in the taxes you will have to pay on your capital gains.

FAQs SWP Calculator

Is the income from an SWP taxable?

Yes. SWP withdrawals are treated as redemptions and are subject to capital gains tax, depending on the type of fund (equity or debt) and the holding period.

Can I stop or modify my SWP?

Absolutely. You have the flexibility to stop, pause, or change the withdrawal amount or frequency of your SWP at any time by submitting a request to the asset management company (AMC).

What is a safe withdrawal rate for an SWP?

A widely discussed rule of thumb is the 4% withdrawal rate, which suggests that you can safely withdraw 4% of your initial corpus each year, adjusted for inflation, without depleting it. However, the ideal rate depends on your age, risk appetite, and market conditions. An SWP calculator can help you model different rates.

Can I set up an SWP in any mutual fund?

Most open-ended mutual fund schemes offer the SWP facility. It is particularly popular in debt funds, balanced advantage funds, and hybrid funds due to their relative stability compared to pure equity funds.

Can I set up an SWP to withdraw only the profits and keep my initial investment untouched?

Yes, you can! This is a popular SWP option often called “Capital Appreciation Withdrawal.” Instead of a fixed amount, you can instruct the fund house to systematically withdraw only the amount equivalent to the capital gains your investment has made over a specific period (like a month or a quarter). This is an excellent strategy for those whose primary goal is to preserve their initial capital while still generating an income stream. However, it’s important to remember that this income will not be fixed; it will depend entirely on the fund’s performance. In months where the fund doesn’t generate a positive return, you won’t have any withdrawal.